Lumen Wealth · Wealth Architecture Advisors

How much do you actually keep? How much will you pass on?

Most high-income families and business owners focus on earning — but few have ever truly calculated: after taxes, risk exposure, and structural inefficiencies, how much actually stays? How much reaches the next generation?

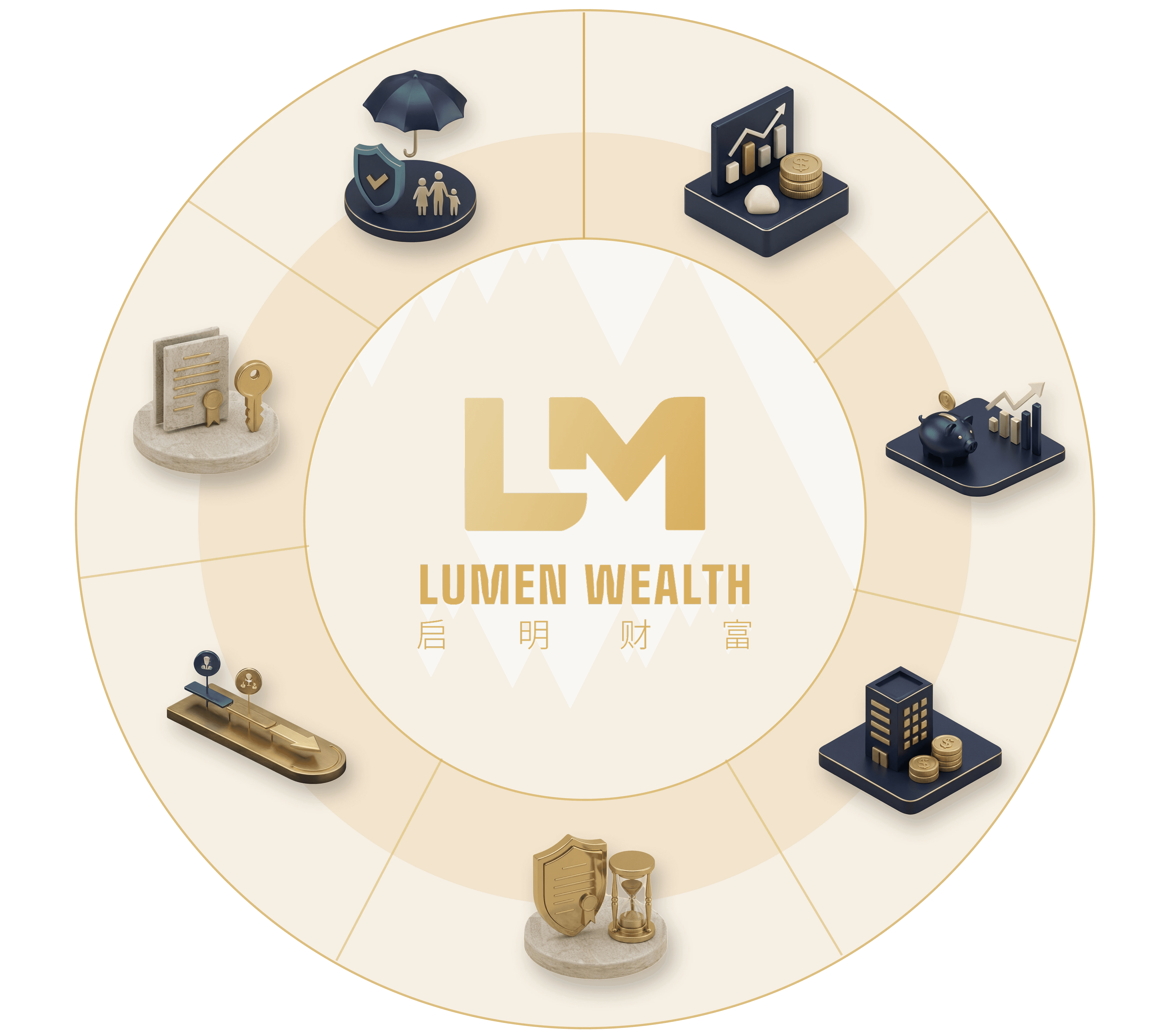

The Solution

We don't fix one piece — we address the entire picture.

Insurance

Succession

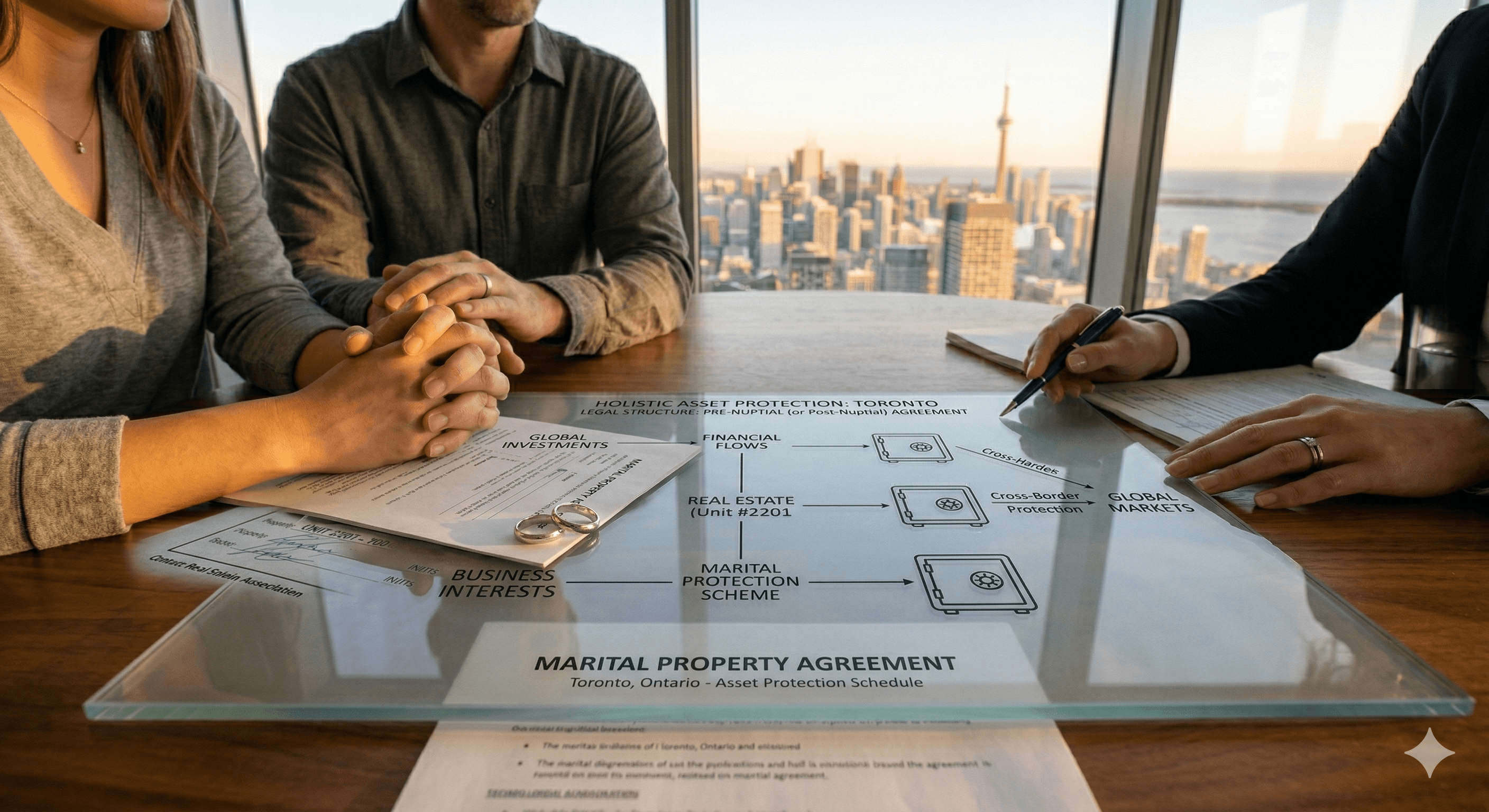

Marriage

Tax on Death

Corporate

Tax

Asset

Who We Serve

If you're one of these people, we can help.

Our Value

From Scattered Pieces to One Complete Picture

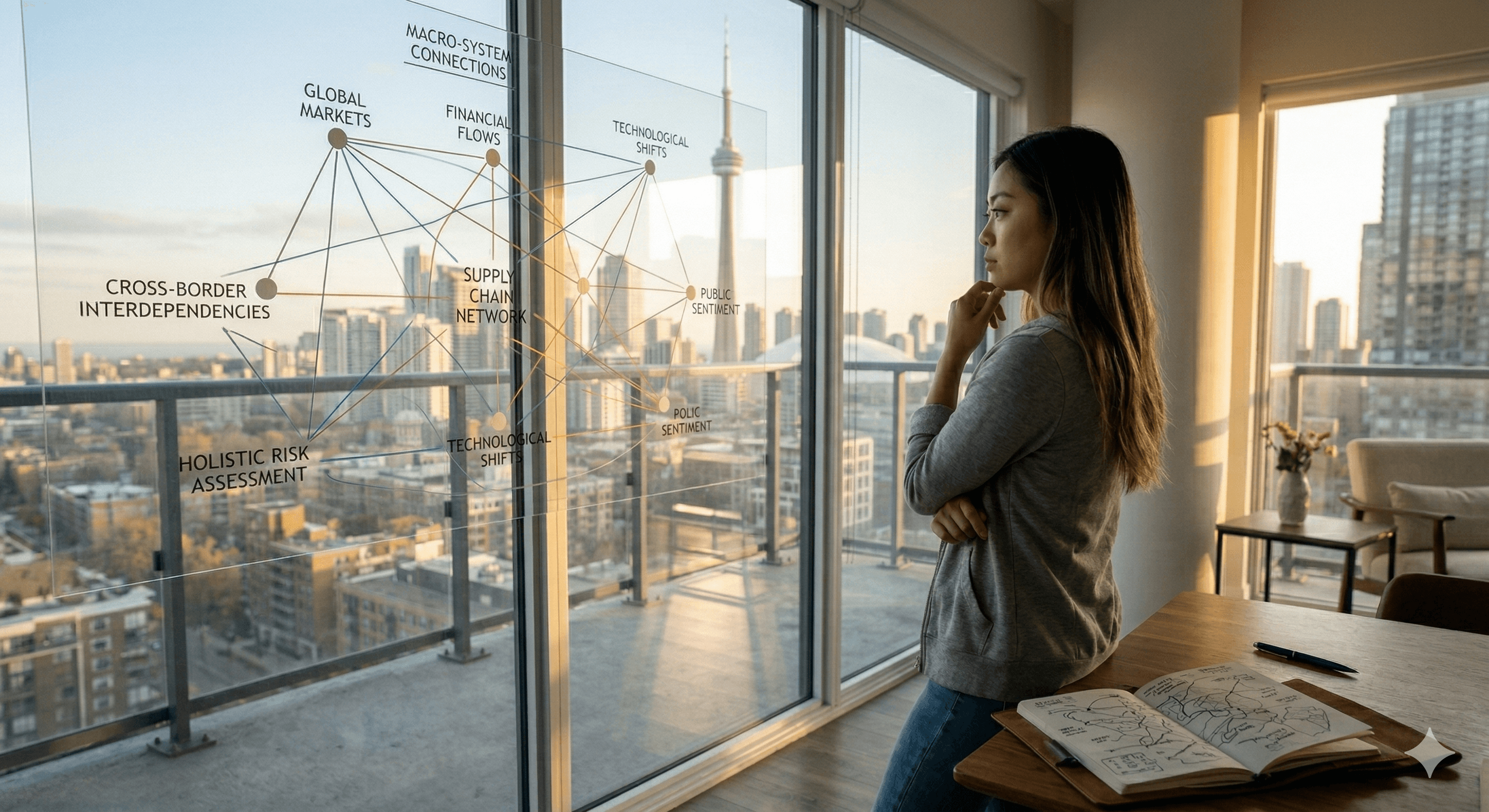

Most people make financial decisions in isolation — housing is separate, the business is separate, insurance is separate. But these decisions are interconnected, and those connections determine how much you ultimately keep and how much you pass on.

We stand at the macro level to help you see the links between asset allocation, account structure, corporate architecture, tax planning, and succession — then design a comprehensive plan where each component is executed by the most qualified professional.

Case Studies

Problems we've solved for our clients

About the Founder

CFA | FRM | JD, University of Toronto

Integrating investment analysis, risk management, and law, Yiming is a rare practitioner in Canada reviewing wealth through both financial and legal lenses. Her foundation includes 15 years in Canadian real estate and a background in BMO Commercial Banking.

Highly skilled advisors often work in silos, leaving critical gaps. When accountants, lawyers, and financial planners don't communicate, tax savings are missed, assets remain exposed, and legal documents contradict one another. These aren't individual failures, but a lack of total-picture coordination.

Lumen Wealth sees the full picture, designs the architecture, and ensures the entire plan is executed.

Tax Law | Trust Law | Commercial Law

Our Process

How We Work

1

Comprehensive Scan

We audit your entire landscape—corporate structure, real estate, insurance, and wills—to identify hidden structural blind spots. This initial, fee-based consultation provides a thorough diagnostic of your assets and core objectives.

11

Architecture Design

Based on our findings, we design a customized master plan. We define critical adjustments, set priorities, and project expected outcomes. This strategy is entirely independent and not tied to any specific product or provider.

111

Implementation

We translate the architecture into specific action items, coordinating with lawyers and accountants to ensure consistency. By overseeing every moving part, we ensure every legal and financial component serves the same unified objective.

Interactive Tool

Upon your passing, how much tax would your company owe?

At passing, corporate shares are deemed disposed, often triggering massive capital gains taxes. Without a plan, your family must raise significant liquidity overnight to settle the bill. Use this tool to estimate your potential liability based on your current corporate asset structure.

For educational purposes only; not tax advice. Please consult a licensed professional for specific matters.

FAQ

Questions You May Have

How are you different from a financial advisor?

Do you provide legal or tax services?

I already have an accountant and a lawyer — do I still need you?

What kind of person is a good fit for your services?

What can a single consultation accomplish?

What regions do you serve?

Reveal the blind spots in your current planning.

A comprehensive scan designed to find the questions no one else is asking.